I am pleased to present a new article, an Editors' Pick, published on Seeking Alpha, regarding OCC

I am pleased to present a recent article, published under my pseudonymous Seeking Alpha handle and chosen by Seeking Alpha's editors as an Editors' Pick, on OCC (Optical Cable Corporation): click here to read. (The article is not behind a paywall, but you might need a free sign in.)

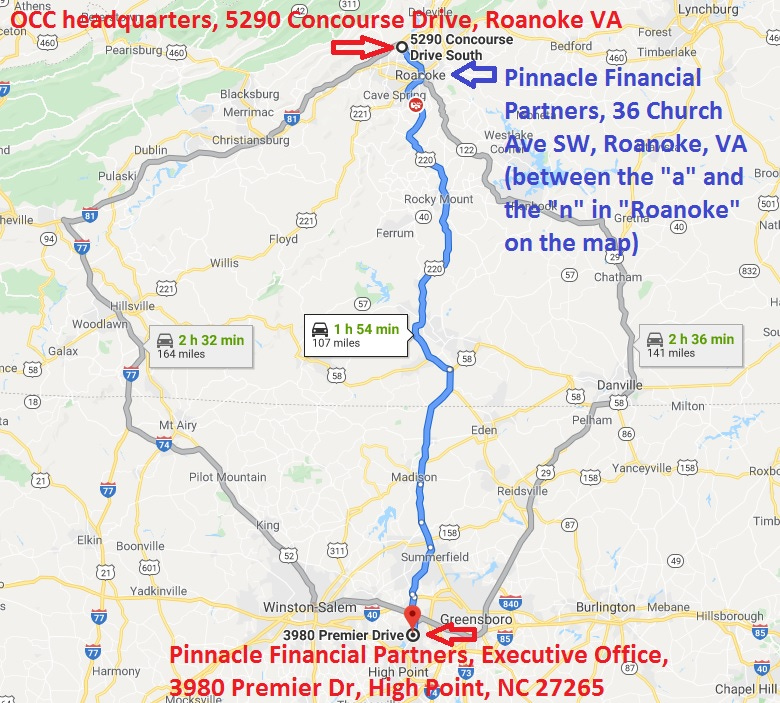

The seventh and most recent loan amendment's signator for Pinnacle Bank is an employee of the bank's High Point, NC office (107 miles from OCC's Roanoke headquarters), rather than the bank's local Roanoke, VA office (7 miles from OCC's headquarters). In contrast, the original 2016 loan and six subsequent amendments were signed by employees of Pinnacle's Roanoke office. Might an out-of-state office offer a clue to something increasingly meaningful? Or might it be a non-event?

I lay out the case that the probability of a sale of OCC to an acquirer seems to have increased. Having fallen short of previously agreed upon bank covenant targets twice in the first three quarters of 2019, if OCC continues to fall short at FY2019-end and possibly into FY2020, OCC may find itself encouraged by its bank to make changes. At the same time, OCC's low stock price may attract interest from potential acquirers (OCC's enterprise value is a bargain at half of projected FY2019 revenues). I make the case that a sale of the company is in the interest of shareholders and also in the self interest of OCC's management. The window is now open for management to be heroes by selling the company.

Normally judging financial self interest is an effective method of forecasting. But of course financial self interest is not emotional self interest. As always, management has a lot of power to determine how things turn out. Pinnacle Bank does as well, if it chooses to exercise it.

Potential faults of my thesis: 1) If Pinnacle agrees to an extension of the revolver, the agreement would take near-term pressure off OCC. But, in my opinion, it still makes sense to sell the company. 2) OCC could refinance the revolver. 3) If 9.99% shareholder Buffett-lieutenant Ted Weschler were to reduce his stake in OCC, the stock would sell off and a powerful advocate for a higher stock price would be sidelined. None of these three scenarios is included in my base case, but any is possible.

(OCC is a tiny company, and the stock difficult to trade, so I am not encouraging any buying or selling of OCC's stock; it is too risky. Disclosure: I own the stock.)