Warren Buffett's amazing Fortune magazine article wears well after 20 years

Buffett took a contrarian stand 20 years ago. Time has proved him prescient.

Tomorrow (November 22, 2019) marks the 20th anniversary of Carol Loomis's 1999 Fortune article featuring Warren Buffett, an article that was distilled from a number of speeches Buffett made that year.

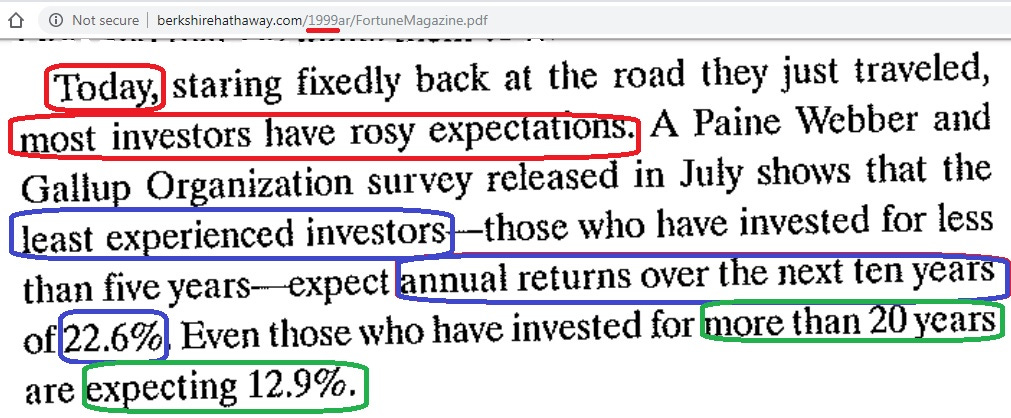

In 1999, as you may recall, investors were reveling in historic stock market returns, and anticipating elevated returns to follow. In 1999, investors who had 20 years of experience were expecting annualized stock market returns over the following 10 years to be 12.9%. Investors with less than 5 years experience were expecting annualized stock market returns to be 22.6%.

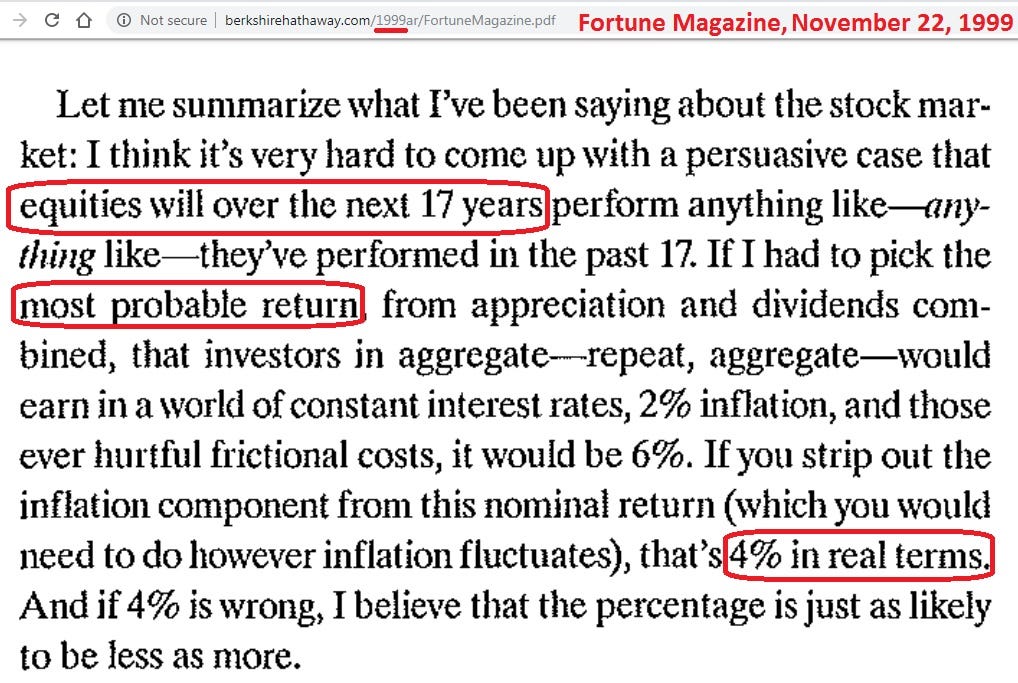

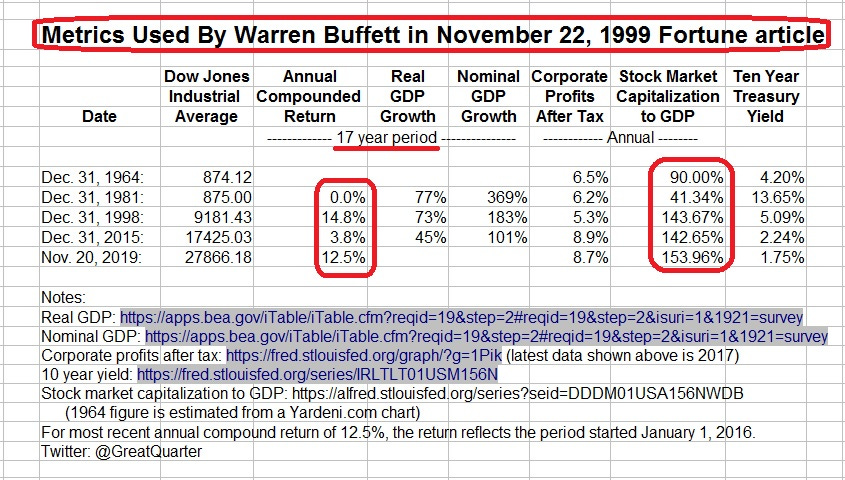

In contrast, Buffett predicted 4% real returns for the seventeen year period December 31, 1998 to December 31, 2015. The nominal price return of the Dow Jones Industrial Average (the index that Buffett used in the 1999 article) for that 17 year period turned out to be 3.8% (see table below), plus dividends which approximated inflation. So, Buffett's prediction of 4% real return was spot on. Amazing!

Back in 1999, Buffett explained stocks could enjoy a higher return during 1998 - 2015 if either:

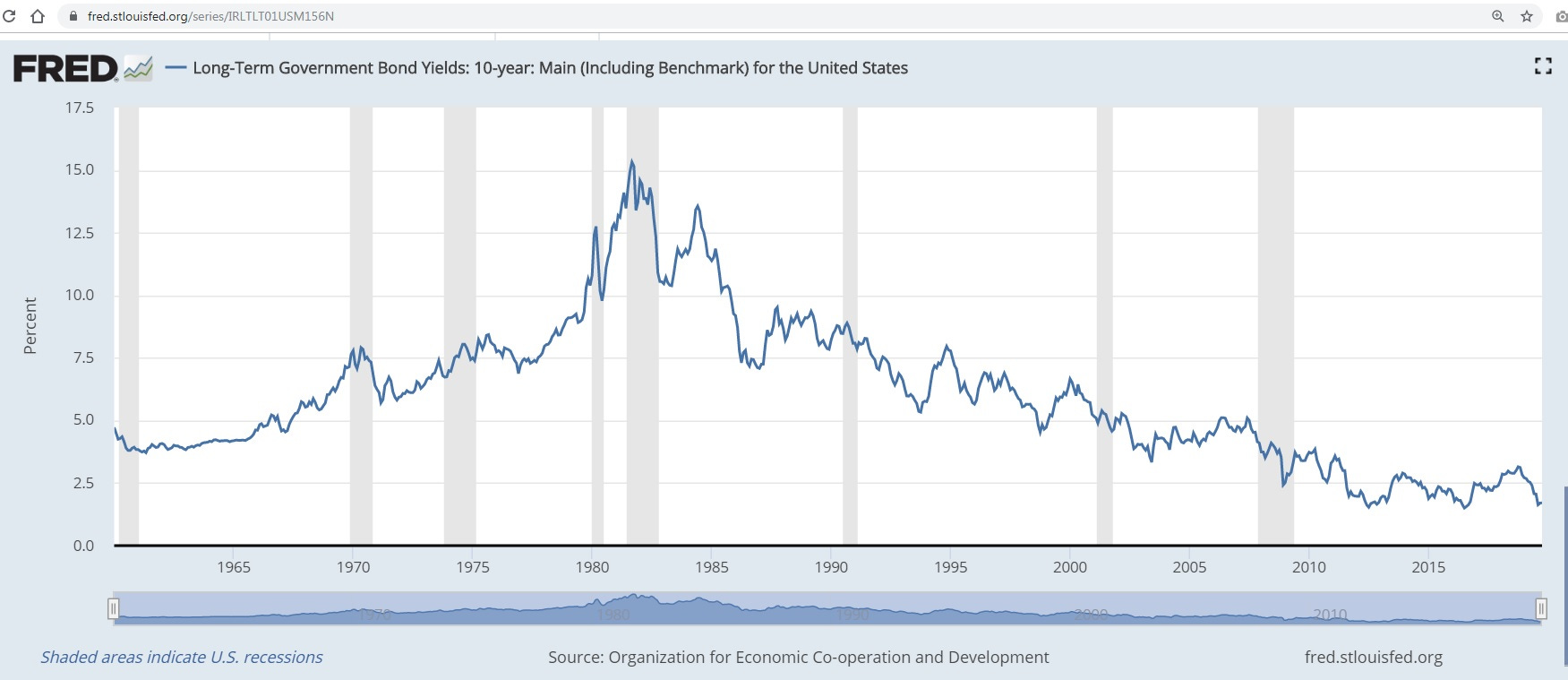

“(1) Interest rates must fall further. If government interest rates, now at a level of about 6%, were to fall to 3%, that factor alone would come close to doubling the value of common stocks.” Rates indeed fell.

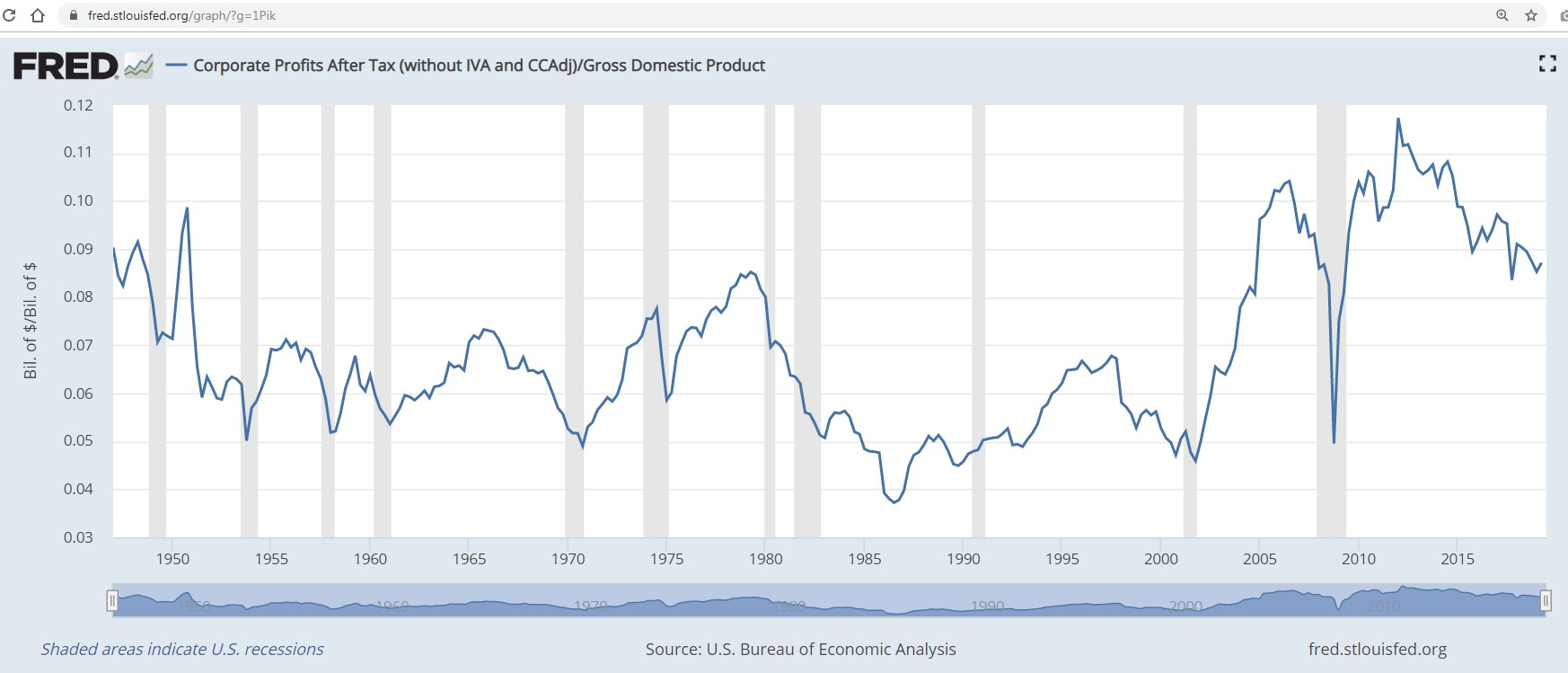

“(2) Corporate profitability in relation to GDP must rise... In my opinion, you have to be wildly optimistic to believe that corporate profits as a percent of GDP can, for any sustained period, hold much above 6%.” Profits indeed rose.

Both bullish scenario #1 and bullish scenario #2 occurred. Interest rates fell to 2.24% (now 1.75%). And corporate profitability as a percent of GDP rose to 8.9% (now, most recent figure: 8.7%).

But even though both #1 and #2 were fulfilled, stocks still went up Buffett's predicted 4% real annualized return (capital gains and dividends, adjusted for inflation).

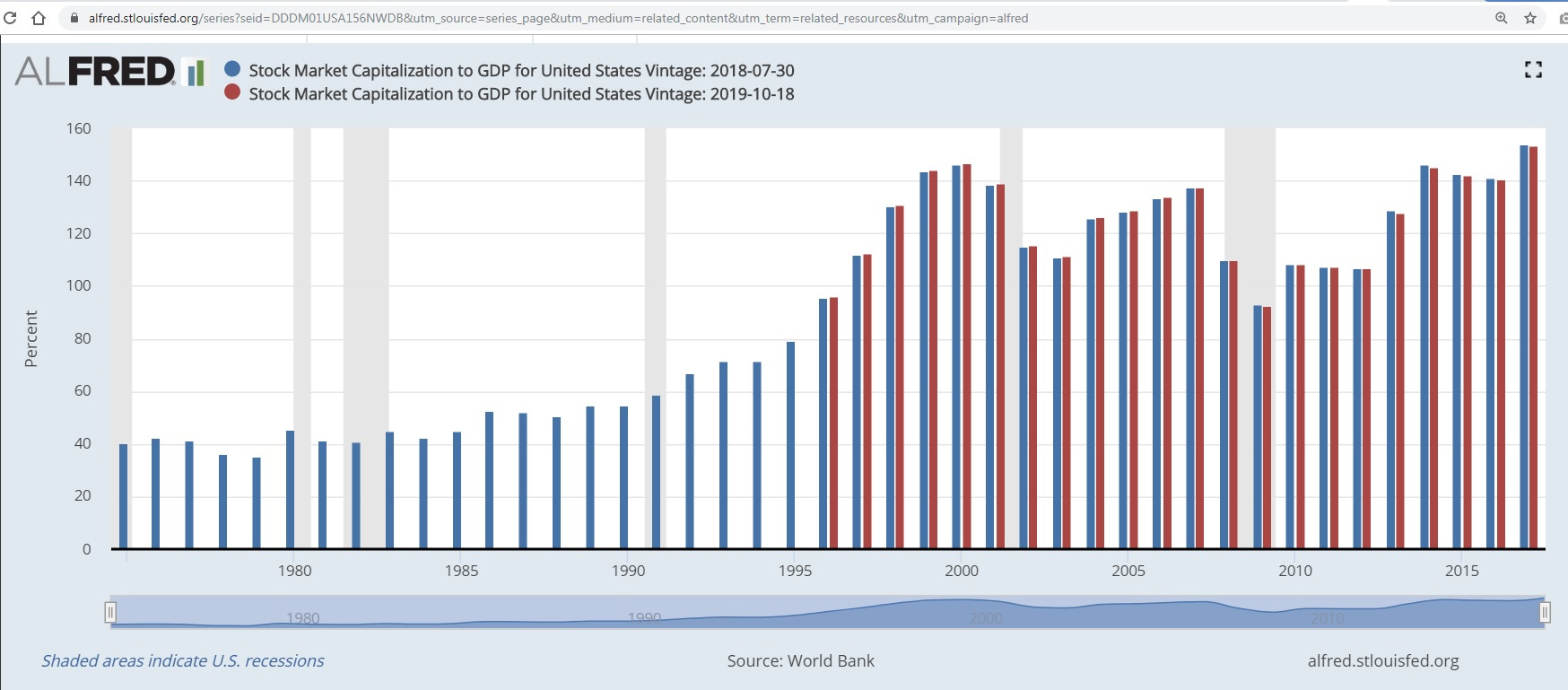

In a 2001 Fortune article with Carol Loomis, Buffett was quoted: “the market value of all publicly traded securities as … a percentage of GNP … is probably the best single measure of where valuations stand at any given moment.”

Note that on December 31, 2015, the stock market capitalization to GDP ratio stood at 142.65%, roughly unchanged from its 1998 level of 143.67%. But when you couple that observation with the corporate profit after-tax as a percentage of GDP, 8.9% in 2015 compared to 5.3% in 1998, you see that corporate profits as a percent of GDP rose 70%. Therefore, on a P/E basis, the stock market in 2015 was much cheaper than in 1988.

But, if profits as a percent of GDP decline to the level Buffett argued was sustainable over the long term – 6% (see #2 above) – stocks are currently way over-valued. (Jonathan Tepper’s and Denise Hearn’s book The Myth of Capitalism helps to explain why corporate profits recently have been meaningfully higher than historical averages.)

Buffett ended his 1999 Fortune article with: “This talk of 17-year periods makes me think – incongruously, I admit – of 17-year locusts. What could a current brood of these critters, scheduled to take flight in 2016, expect to encounter?”

Does Buffett's “take flight” image suggest Buffett expected a new big bull market to start on December 31, 2015?

If the first four-year return of the new 17-year cycle continues at the same 12.5% annualized return pace, the Dow Jones Industrial Average will end 2032 over 129000. (That is not a prediction, just math.)

Back in 1999, Buffett said: “So where do some reasonable assumptions lead us? Let's say that GDP grows at an average 5% a year--3% real growth, which is pretty darn good, plus 2% inflation. If GDP grows at 5%, and you don't have some help from interest rates, the aggregate value of equities is not going to grow a whole lot more. Yes, you can add on a bit of return from dividends.” Note that Buffett's simple 3-factor model starts with: 1) an assumption regarding GDP, then adding in assumptions about: 2) corporate profits as a percent of GDP, and then assuming: 3) an interest rate used to discount future profits.

During the period December 31, 1998 to December 31, 2015, US investors got the 4% real return the Buffett predicted in the 1999 Fortune article. But US investors got a lot more in terms of a set-up for future returns beyond 2015: 1) much lower interest rates, and 2) much higher profits as a percent of GDP. But, while the US stock market is not as expensive as it was in 1999, neither is it as cheap as it was in 1981. Maybe we can enjoy a big bull market until 2032 (punctuated with bear markets of course)? Who knows?

If you like this Substack post, please sign up for future posts to be delivered to you via email, for free.

Or share this post.

Appendix A

International markets look interesting.

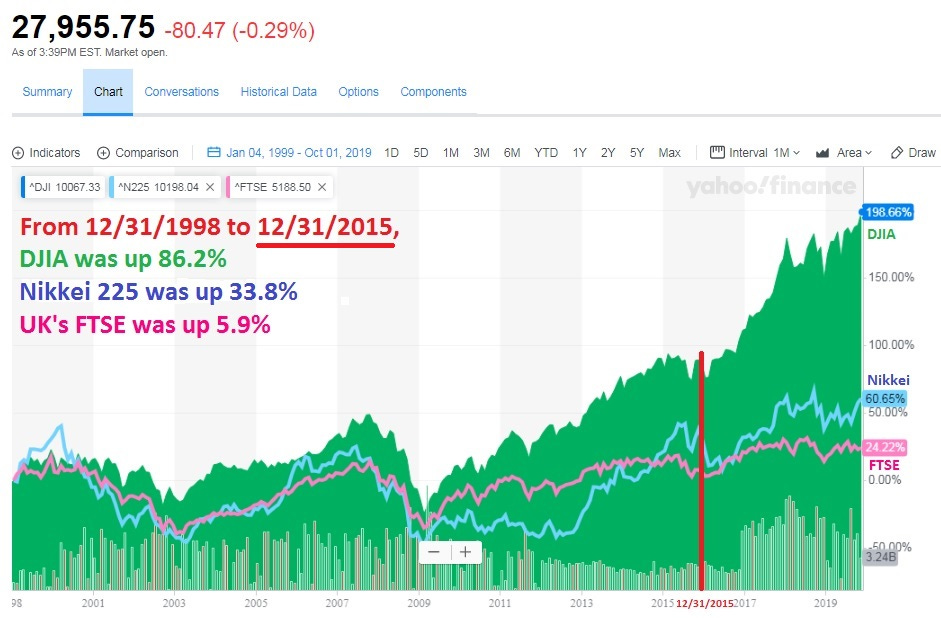

The Dow Jones Industrial Average (the index Buffett used in the 1999 Fortune article) was up 86% from December, 1998 to December, 2015.

In contrast, the UK's FTSE index was up only 5.9% in price during 1998-2015 (now 20.2% from December 31, 1998). 5.9% over 17 years, not annualized. But, the UK is being buffeted by political turmoil in the form of Brexit and potentially the upcoming December 12, 2019 election. A “bad” election result might not be discounted.

The Japanese Nikkei was up only 33.8% in price during 1998-2015 (now 60.6% from December 31, 1998). The Nikkei, which reached a 38,915 high in 1989, is now 23,038.58.

Appendix B

Warren Buffett & Carol Loomis Fortune articles:

Warren Buffett/Carol Loomis Fortune article November 22, 1999: http://www.berkshirehathaway.com/1999ar/FortuneMagazine.pdf

Warren Buffett/Carol Loomis Fortune follow-up 2001:https://archive.fortune.com/magazines/fortune/fortune_archive/2001/12/10/314691/index.htm

Carol Loomis Fortune follow up at 17 years, November 22, 2016:https://fortune.com/2016/11/22/surprise-warren-buffett-turns-out-to-be-more-prescient-about-stocks-than-politics/