Should we focus on expectations for '20 or for the 20s?

Will the 2020s be the Roaring Twenties, again?

Human nature is endearing.

We are generally optimistic, to a fault at times.

I was excited my new business cards arrived, as 2020 approached.

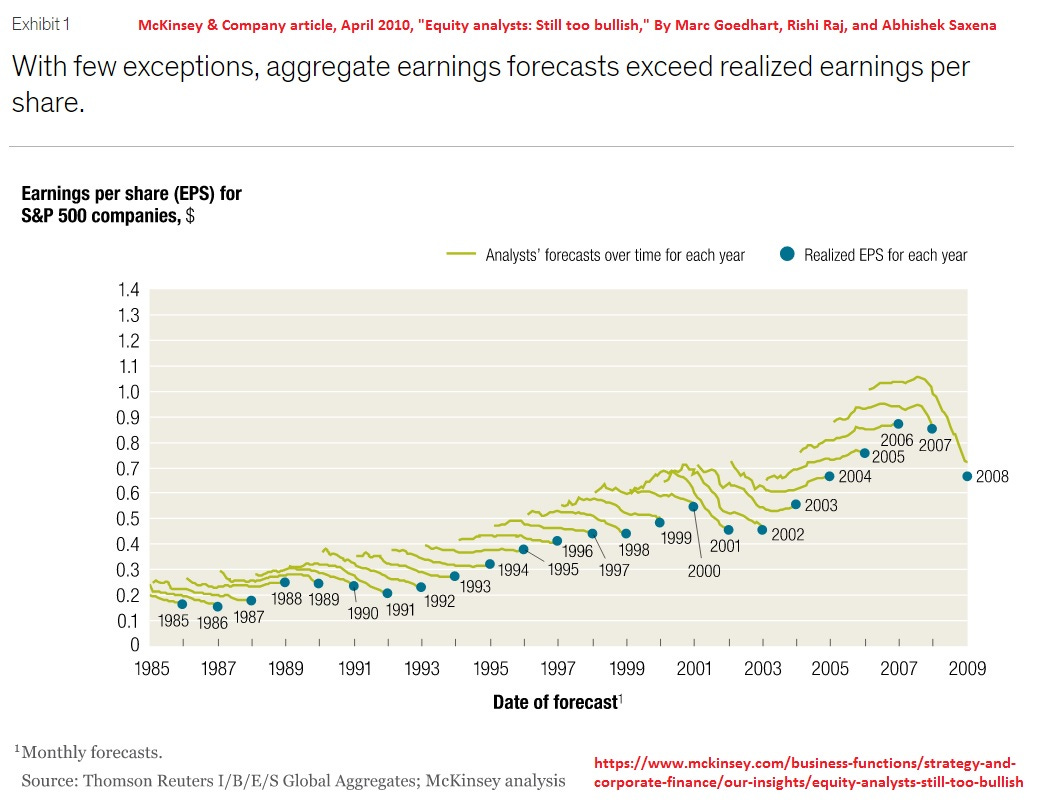

But then I read a McKinsey & Company article, from April, 2010, entitled "Equity analysts: Still too bullish," by Marc Goedhart, Rishi Raj, and Abhishek Saxena.

In the twenty five year chart above, it appears that twice (2005 and 2006) the realized EPS exceeded the beginning of the year forecast. We are reminded, once again, that the future does not necessarily fulfill our optimistic hopes.

Having been trained as a high yield analyst, I find it helpful to consider the perceived worst case and evaluate whether that worst case is manageable. If it is, you might have a good investment.

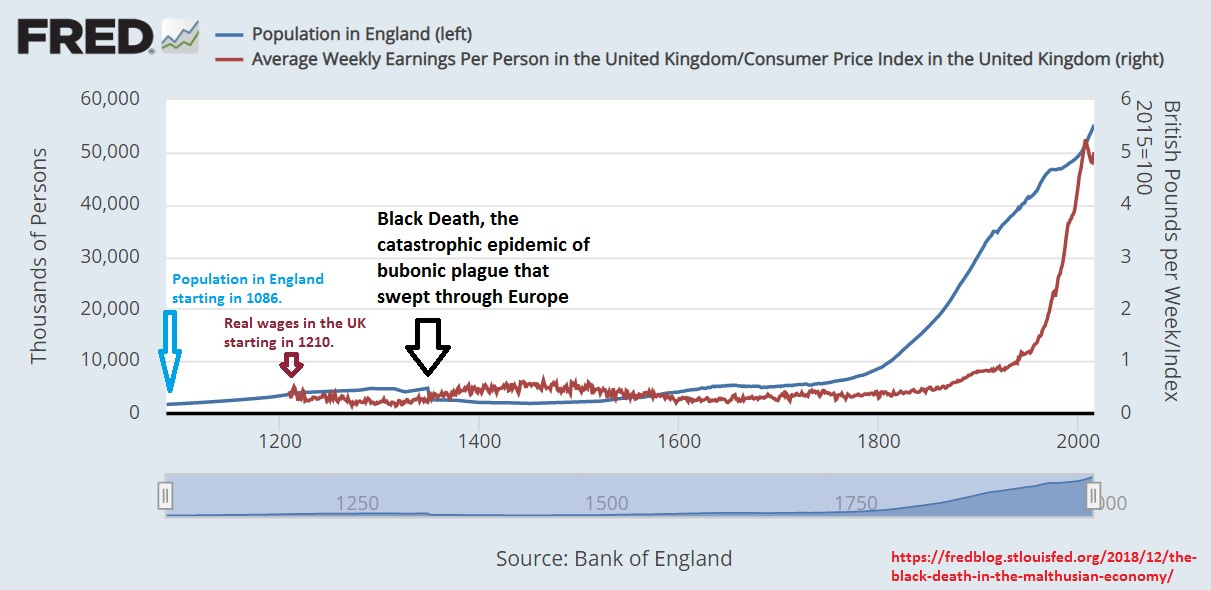

As an aid in that exercise, I reviewed past economic history. Back to 1086 England. FRED (Federal Reserve Economic Data, via the Federal Reserve Bank of St. Louis), through the Bank of England, has data on the population in England and real wages in the United Kingdom, starting in 1086 and 1210, respectively. A good place to start.

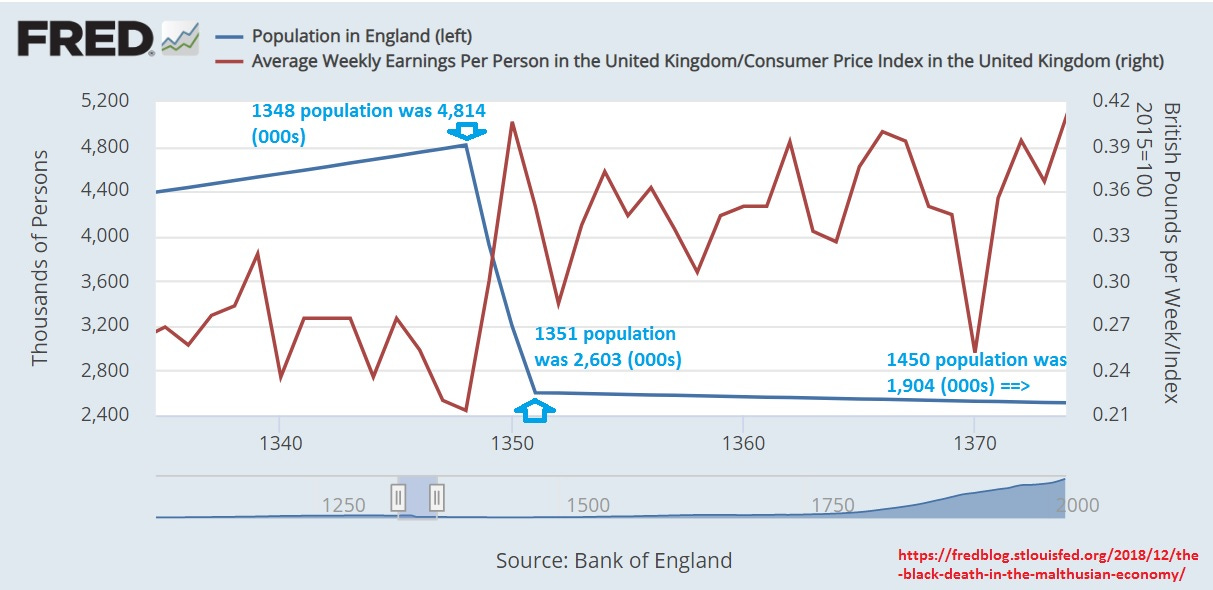

With the aid of FRED’s article titled “The Black Death in the Malthusian economy,” and subtitled “A glimmer of wage growth in the Dark Ages,” I noted that the population of England declined from 4,814,000 inhabitants in 1348 to 2,603,000 in 1351. England’s population continued to decline to 1,904,000 in 1450, according to the Bank of England. Wow!

But note the red line, which represents an index of Real Average Weekly Earnings Per Person/CPI. With the decline in population, the supply/demand for labor shifted, and real wages increased.

This sudden and massive drop in population is the Black Death, the catastrophic epidemic of bubonic plague that swept through Europe. Notice something else that is quite particular about this period: Real wages went up substantially and clearly stayed higher for a while. This is very different from the period since the Industrial Revolution, where both wages and population have moved in the same direction.

The discussion of the so-called Malthusian equilibrium is beyond the scope of this post, but you can read the fascinating article on FRED’s website.

We have seen even a worst case could bring moderating benefits. More importantly, we see the increase in the standard of living since the mid-1800s has been stunning.

To review, McKinsey showed Wall Street analysts start with high earnings estimates and usually lower estimates as the year progresses. What if we humans are too optimistic with respect to next year but not sufficiently optimistic with respect to longer periods?

“People tend to overestimate what can be done in one year and to underestimate what can be done in five or ten years.” (From the 1965 book “Libraries of the Future” by J. C. R. Licklider.)

Perhaps it is the same with analysts. We overestimate the near future and underestimate the distant future.

Billions of people go to work every day. During each work day, some people make small improvements (process improvements, technological advances, etc). Periodically, someone makes a gigantic improvement, such as a world-changing invention. Quality of life improves for everyone, albeit unevenly. Broadly, the stock market reflects that improvement over time, with leads and lags. Barring an outside force that could change the dynamic, like a global war (a disaster), more of the same seems likely in the future.

What about the S&P return for next year?

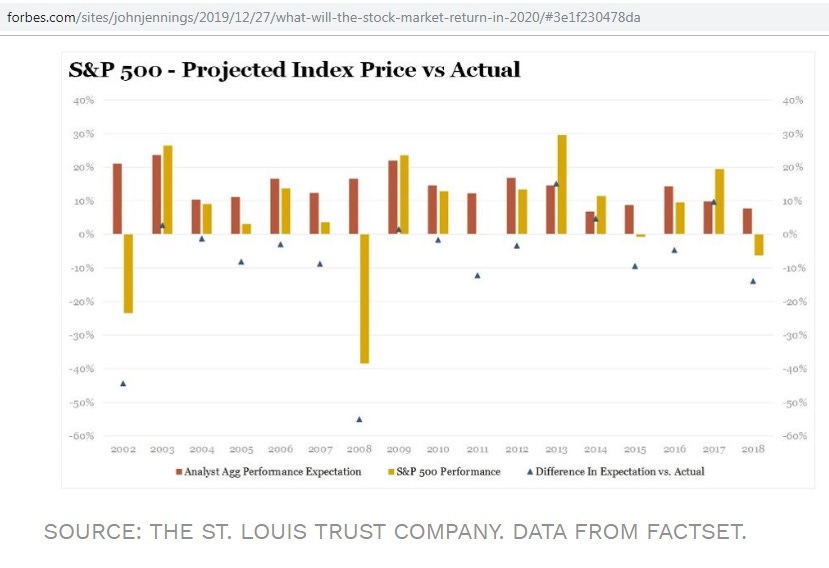

Rick Rieder, BlackRock’s global fixed income CIO, tweeted about historical instances of S&P performance in the year following a 20% S&P return.

Given the moderate #economic backdrop that we’ve outlined for 2020, can risk #assets continue to perform into next year? There are historical examples of strong back-to-back year repeat performance in #equities…

The results should be encouraging to “risk asset” bulls:

If I had to project S&P returns for 2020, I would do what all the high-paid strategists seem to do: calculate the long term average return, adjust it by a percent or two depending on how one feels, knock off a percentage point to adjust for optimistic bias, and then develop reams of data that support your conclusion. Using that logic, and taking about 30 seconds, my cynical Great Quarter™ 2020 S&P 500 projected return is 7% (inclusive of a projected 1.8% dividend yield), with lots of price volatility. Consequently, the Great Quarter™ Year-End 2020 S&P 500 price target is 3399. (These projections are worthless.)

Ironically, predicting stock prices over the long term might be as valid as predicting stocks over the next year.

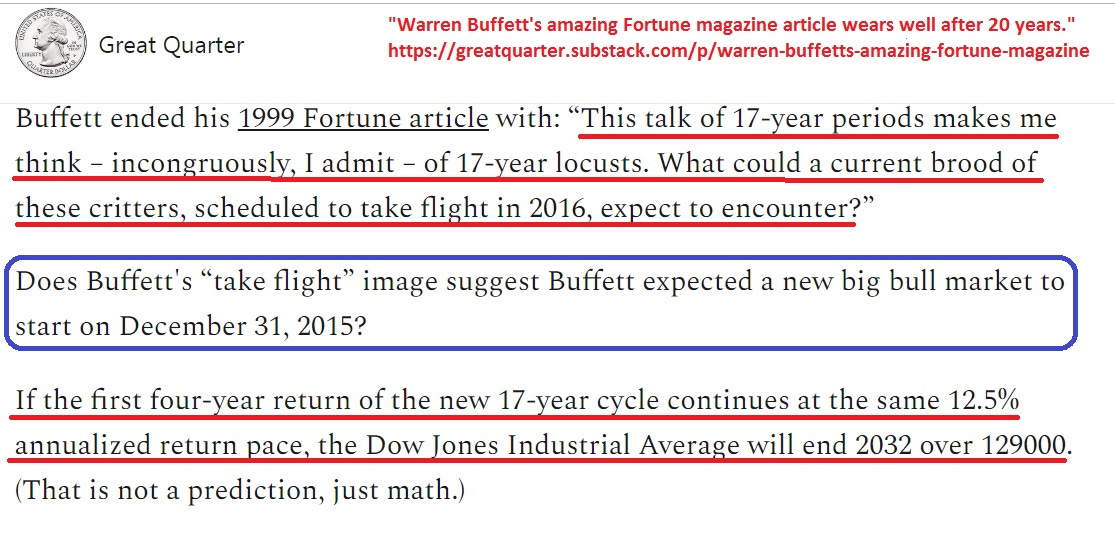

Modeling Buffett’s thought process in my substack post “Warren Buffett's amazing Fortune magazine article wears well after 20 years,” my 2032 projection for the Dow Jones Industrials (the index Buffett used in his 1999 Fortune article with Carol Loomis) was 129000. Is that a better projection than the 6% return projection for 2020? Both projections are meaningless, but they both might be right. Time will tell.

In closing, we can’t say 2020 can’t be worse 2019 (it can). But we can say there are billions of people going to work today; some will make small improvements today; some will make big improvements today. Over the long run, even with ups and downs caused by booms and recessions, and stock market overvaluations and undervaluations, stocks should roughly reflect an anticipated generally improving economy.

🎆 Happy New Year! 🎆

As we contemplate the new year and the new decade, please remember:

every quarter is a great quarter!

The Great Quarter Giveaway™ has been extended until January 31, 2020 at 11:59pm Eastern or one hundred Great Quarters™ have been claimed. Aside from the expiration, all other terms are the same as in the December 21, 2019 substack post.

Feel free to comment to this post. Scroll down to comment section.

To contact me, either: 1) reply to this email; or, 2) direct message me on twitter.

If you favor the Great Quarter™ brand, visit Great Quarter’s twitter for short form, Great Quarter’s substack for medium form, and Great Quarter’s Seeking Alpha for long form company-specific research.

To share this post:

To sign up for free, infrequent Great Quarter substack emails:

✓

To follow Great Quarter on twitter: